Joint statement on the European Commission’s Grids Package

The European Commission’s Grids Package represents an important step towards placing energy infrastructure at the core of Europe’s transition towards affordable, competitive, and secure energy. By strengthening the framework for planning, permitting, financing, and operating cross-sector energy networks, the package aims to contribute to the objectives of the Commission’s Action Plan for Affordable Energy and Europe’s broader industrial and climate ambitions.

Hydrogen infrastructure – which includes transmission, distribution and geographically confined hydrogen networks, as well as storage and terminal facilities – is a critical pillar of Europe’s decarbonised energy system. The infrastructure will also be instrumental in providing low-carbon and renewable hydrogen to industry as feedstock for current and future hydrogen users.

With the right infrastructure in place, hydrogen can contribute to decarbonisation of industry and other sectors, reduce renewable electricity curtailment, support system flexibility, provide large-scale long-term energy storage and enable the integration of variable renewable energy sources across sectors, where electrification alone may be insufficient to address peak demand and system constraints.

However, unlocking this potential requires a regulatory and financial framework that fully reflects the specific characteristics and maturity level of the hydrogen sector. Indeed, hydrogen market and its underlying backbone is an emerging one that will develop progressively, combining large-scale transport infrastructure with decentralised distribution infrastructure that support early demand, system integration and market uptake.

While the co-signatories of this statement welcome the EU Grids Package, several elements require further refinement to ensure that hydrogen infrastructure can be deployed at adequate scale, at speed, and at an acceptable level of risk for investors and consumers.

1. Offshore and EU-level planning: the need for a more comprehensive and inclusive approach towards hydrogen infrastructure planning

The ambition to strengthen offshore network planning is welcomed. However, hydrogen infrastructure must be fully integrated into offshore planning frameworks and coherently linked to onshore infrastructure development. This is to ensure timely connections to demand centres and to avoid interface bottlenecks between production, transport, distribution and end use. In this context, ENNOH should be placed on an equal footing with ENTSO-E in the governance and development of offshore network planning. Given the likely increasing relevance of offshore hydrogen production and transport, ENNOH’s co-authorship when it comes to offshore network development plans is essential to ensure coherent, technology-neutral, and forward-looking infrastructure planning.

In addition, the role of storage sites and terminals in EU-level infrastructure processes, including in the TYNDP and the elaboration of the joint scenario, should be clearly strengthened. These scenarios and planning exercises should take comprehensive account of all relevant infrastructure components and be firmly based on the expertise, experience and technical capabilities developed over the last two decades by TSOs and HNOs, in cooperation with storage, terminal and distribution operators.

Furthermore, with regards to the TYNDP process, the EU DSO Entity should have a defined and meaningful role beyond consultation, including in the provision of data and input to ensure that planning assumptions properly reflect local system realities.

2. Cross-border cost allocation (CBCA): prioritising de-risking

Cross-border cost allocation mechanisms play an important role in enabling deployment of European cross-border infrastructure projects. However, for hydrogen infrastructure in particular, reliance on CBCA methodologies risks slowing down or outright preventing hydrogen backbone buildup. CBCA methodologies have been developed for mature gas and electricity markets, and therefore, they cannot be simply duplicated and applied to the emerging hydrogen market.

Limited demand visibility in the early stages of the hydrogen market development increases investment uncertainty. In this context, rigid CBCA approaches applied to hydrogen projects may lead to disproportionate cost allocation and increased financial risk for hydrogen infrastructure projects. Rather than prioritising increasingly complex CBCA methodologies, the regulatory framework should place greater emphasis on effective de-risking tools, including risk-sharing mechanisms, targeted financial instruments, and coordinated support at European and national levels.

Such tools are essential to unlock early-stage hydrogen infrastructure investments and to ensure that cross-border projects can reach final investment decisions. This is particularly relevant given the diversity of hydrogen infrastructure project profiles, ranging from large cross-border corridors to smaller, phased developments happening at local or clusters level.

3. Electrolyser eligibility for Projects of Common Interest (PCI) and Projects of Mutual Interest (PMI)

Serious concerns are raised regarding the proposed increase of the electrolyser capacity threshold in Annex II of the TEN-E framework from 50 MW to 500 MW for eligibility under the PCI regime. A threshold of 500 MW risks excluding a large share of viable hydrogen projects, including phased developments, industrial clusters, and regional hubs that are critical for the gradual build-up of the hydrogen market. This change may inadvertently favour a limited number of large-scale projects while slowing down broader deployment of hydrogen infrastructure across Europe.

A more proportionate and flexible approach to electrolyser eligibility criteria is therefore needed – one that will be better aligned with the current stage of market development.

4. Permitting: equal footing with electricity infrastructure

The objective of accelerating permitting procedures for strategic energy infrastructure is strongly supported. However, hydrogen infrastructure is not yet granted the same level of regulatory prioritisation as electricity infrastructure. In particular, the explicit exclusion of hydrogen storage from streamlined permitting procedures creates a structural bottleneck in the development of an integrated hydrogen system. Hydrogen storage is a critical component of system flexibility, security of supply, and sector integration, and should therefore benefit from accelerated permitting on an equal basis with electricity infrastructure.

Hydrogen infrastructure – including electrolysers, storage, pipelines, and import-related facilities – should be fully integrated into streamlined permitting frameworks and benefit from a clear presumption of overriding public interest where appropriate, similarly to EU permitting processes for electricity projects.

5. Energy Highways initiative: consistent support for all hydrogen corridors

A timely and coordinated political backing of hydrogen corridors is essential to sustain momentum in the development of a truly integrated European hydrogen network. Such support plays a key role in reducing investment risk, enhancing visibility for projects of European relevance and enabling timely infrastructure development in line with system needs.

All hydrogen import corridors identified and promoted by network operators at European level should be supported in a consistent manner, on the basis of transparent, objective and non-discriminatory criteria, to avoid the risk of arbitrary differentiation or inefficient allocation of resources. Such a renewed and coherent political backing of all corridors, based on clear, strategic, economic and technical considerations, would contribute to maximising overall system benefits, reinforcing market confidence and ensuring an efficient deployment of hydrogen infrastructure across the Union. The upcoming revision of the European Hydrogen Strategy could be a natural vehicle to ensure a consistent political framing across corridors.

Signatories

- Publications

- News

- Events

IOGP Europe’s response to the Public consultation on the renewable energy framework (post-2030 RED) for the decade ahead

Joint Letter: Delivering Europe’s Hydrogen Ambitions – Joint Industry Roadmap Ahead of the First European Hydrogen Forum

IOGP Europe calls for simplification of the hydrogen regulatory framework through the Omnibus Package

Recommendations on the proposed new EU funding architecture under the MFF (2028-2034)

IOGP Europe’s response to the call for evidence on the General Block Exemption Regulation (GBER)

Ten action points for a Hydrogen Grids Strategy

IOGP Europe’s response to Draft T&Cs for the H2 Bank third auction

The Mediterranean: an energy and decarbonization opportunity for Europe

IOGP Europe views on the Grids Package

IOGP Europe response to consultation on the Industrial Decarbonisation Accelerator Act (IDAA) and call for evidence

Joint statement: Urgent need for European Commission to correct course on the draft Delegated Regulation on Low Carbon Fuels

The upcoming Grids Package: a critical opportunity not to be missed for the deployment of a European hydrogen infrastructure

Unlocking the Black Sea’s Strategic Energy Potential

EU Hydrogen Strategy needs a fundamental reset

Response to the European Commission’s consultation on the draft Clean Industrial Deal State Aid Framework (CISAF)

Public consultation on inter-temporal cost allocation mechanisms (ICA) for financing hydrogen infrastructure

Joint Statement: Call for action- Urgent need to recognise third country exports of gaseous fuels under the Union Database

Advancing a Competitive, Resilient, and Integrated Energy Market

Joint Statement: Reality Check for European Hydrogen Policy to Adjust the Course

The Case for a European CCS Bank

The Joint Statement on the Low-Carbon Fuels certification draft Delegated Act

IOGP response to the public consultation on the draft Methodology to determine the greenhouse gas (GHG) emission savings of low-carbon fuels

Joint Statement on the Low-Carbon Fuels certification Delegated Act

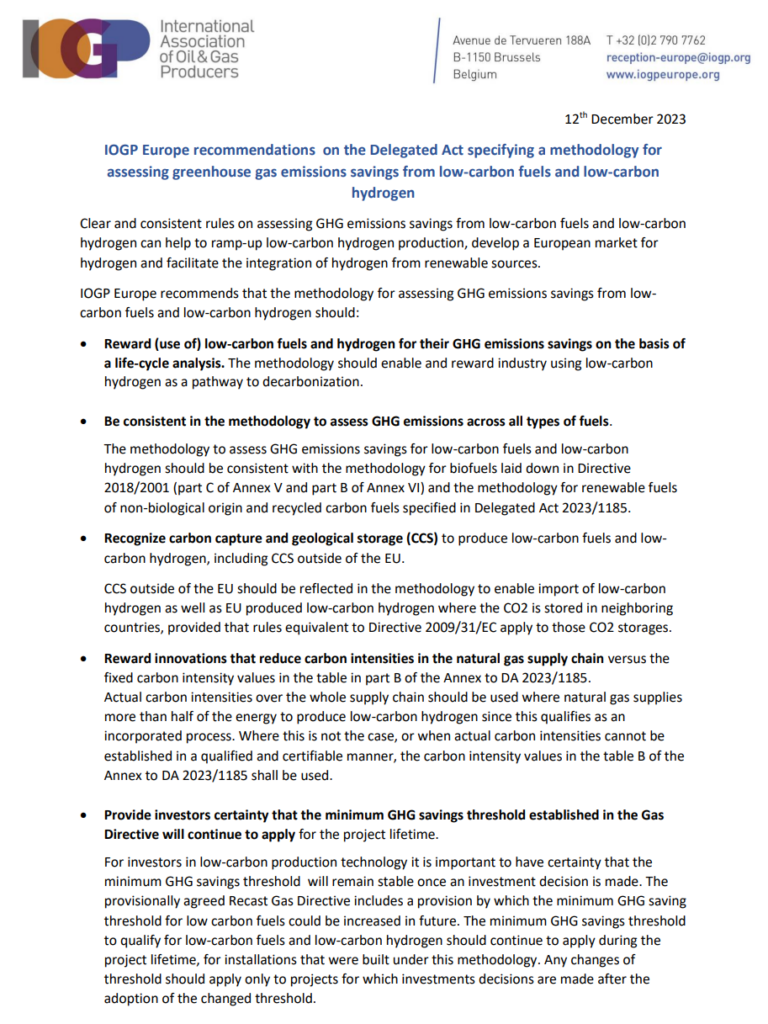

IOGP Europe recommendations on the Delegated Act specifying a methodology for assessing GHG emissions savings from low-carbon fuels and low-carbon hydrogen

IOGP position paper on the European Commission’s public consultation on the EU climate target for 2040

IOGP position on capital requirements

IOGP response on Competitive Bidding schemes for hydrogen under the Innovation Fund

IOGP response on revamping the Strategic Energy Technology (SET) Plan

IOGP response to the public consultation on the Hydrogen and Decarbonized Gas Market package

IOGP comments to R. W. Howarth and M. Z. Jacobson (2021): How Green is Blue Hydrogen?

IOGP response to the public consultation on the Renewable Energy Directive (RED) proposal

IOGP response to public consultation on the revised Climate, Energy and Environmental Aid Guidelines (CEEAG)

IOGP Paper on metric to use for 2030 targets

IOGP input to the consultation on the Hydrogen and Gas Market Decarbonization Package

Response to consultation on costs of implementing MRV regulation based on OGMP

IOGP response to the roadmap on the modification of the General Block Exemption Regulation (GBER)

IOGP response to the roadmap and inception impact assessment concerning revision of the 3rd Gas Package

IOGP written input to the consultation “Maritime sector – a green post-COVID future”

What’s Right? What’s Wrong? IOGP comments on the ‘EU Strategy for Energy System Integration’ and ‘A hydrogen strategy for a climate neutral Europe’

IOGP response to the inception impact assessment concerning the revision of the 2018 Renewable Energy Directive (REDII)

IOGP response to the public consultation on the revision of Regulation (EU) 347/2013 on guidelines for TEN-E Regulation

IOGP response to targeted consultation on the revision of Regulation (EU) 347/2013 on guidelines for TEN-E Regulation

IOGP input to the Roadmap on the EU Smart System Integration

IOGP input to the Roadmap on the EU strategy on hydrogen in Europe

IOGP feedback to the Combined Evaluation Roadmap/Inception Impact Assessment on the revision of Regulation (EU) 347/2013 on guidelines for TEN-E

IOGP input to the forthcoming EU Strategy for Energy System Integration

IOGP assessment of National Energy and Climate Plans

Scaling up Hydrogen in Europe

Hydrogen for Europe Pre-study – Key findings

IOGP assessment of draft National Energy and Climate Plans

Hydrogen for Europe

New Pact for the Mediterranean: an opportunity to foster the region’s energy integration

EU Low-Carbon Hydrogen production rules are not the signal investors were waiting for

Press release: 2040 Climate trajectory requires urgent action on policy enablers

Press release: State Aid Framework for Clean Industrial Deal marks a turn towards pragmatic decarbonization

Press release: Low-carbon fuels methodology envisaged by the Commission will block key hydrogen production pathways

Draghi Report: a pragmatic pathway to Competitiveness, Sustainability, and Resilience

Letter: IOGP Europe recommendations on the Hydrogen and Decarbonized Gas Market Package

Letter: Open, inclusive, and pragmatic Green Deal Industrial Plan for Europe

Gas market reform marks a step change in EU approach to the transition

New Re-Stream study assesses the feasibility of transport of hydrogen and CO2 in European gas and oil infrastructure

Letter: Call for a technology-inclusive revision of the TEN-E Regulation

“Hydrogen for Europe” study launch

Towards greater hydrogen production capacity in Europe

Letter: IOGP input on the European Commission’s consultation on the priority list for the development of gas network codes and guidelines for 2021 (and beyond)

Council’s inclusive approach to hydrogen sends strong signal ahead of key legislative year

EU’s hydrogen and energy system vision can only succeed with a more balanced, inclusive approach

Wide industry coalition call for a Hydrogen Strategy inclusive of all clean hydrogen pathways

Hydrogen for Europe: 1st Working Group Meeting

The Europe CCUS & Hydrogen Decarbonisation Summit

Re-Stream Study Launch Event

Hydrogen4EU Launch Event

Sustainable finance: investor, oil and gas sector and global perspectives

Carbon Management Webinars

Sustainable finance: non-financial disclosure for the oil and gas sector and EU taxonomy in practice