IOGP input to the IIA on the EC’s Delegated Regulation on taxonomy-related disclosures by undertakings reporting non-financial information

This document provides IOGP’s input to the Impact Inception Assessment on the European Commission’s Delegated Regulation on taxonomy-related disclosures by undertakings reporting non-financial information.

Context

Reporting on taxonomy-compliant activities will require companies to review their processes and establish new systems and reporting functionalities. The new requirements will likely create additional external and internal costs.

IOGP fully recognises the necessity to advance measures to drive the sustainable transition. However, to ensure that the Taxonomy Regulation works in practice and will achieve its objectives, we call on the European and national authorities to support the industry in the implementation and enforcement of these very new rules and requirements.

Key Points

- One of the options to ensure flexibility is to extend the timeline for the disclosure obligation or retain the principal of one or two pilot years. This phased-in approach could be deployed until all delegated acts on six environmental objectives are adopted by the EU institutions

- Alignment across existing and upcoming legislation is key: we call on the Commission to introduce a clear policy planning framework with well-sequenced, realistic timelines

- The upcoming delegated act should focus on minimum requirements, rather than being too prescriptive and potentially duplicating indicators

- Transitional activities play a crucial role in helping the EU deliver its climate and energy objectives: clear guidelines for the reporting on transitional activities should be provided

- We call on the Commission to carry out a detailed and guided-by-experience impact assessment, and we encourage the Commission to reflect on the “‘One-In, One-Out’ (OIOO) principle “to cut red tape” in the upcoming impact assessment

Overview

- Introduction

- Set workable timelines to achieve comprehensible reports

- Ensure coherence between different tools

- Adopt a flexible approach and include indicators for specific transitional activities

- Adequate impact assessment and adherence to the Better Regulation principles need to be guaranteed

- Final remarks

- Publications

- News

- Events

IOGP Europe position on Industrial Accelerator Act and recommendations for modifications

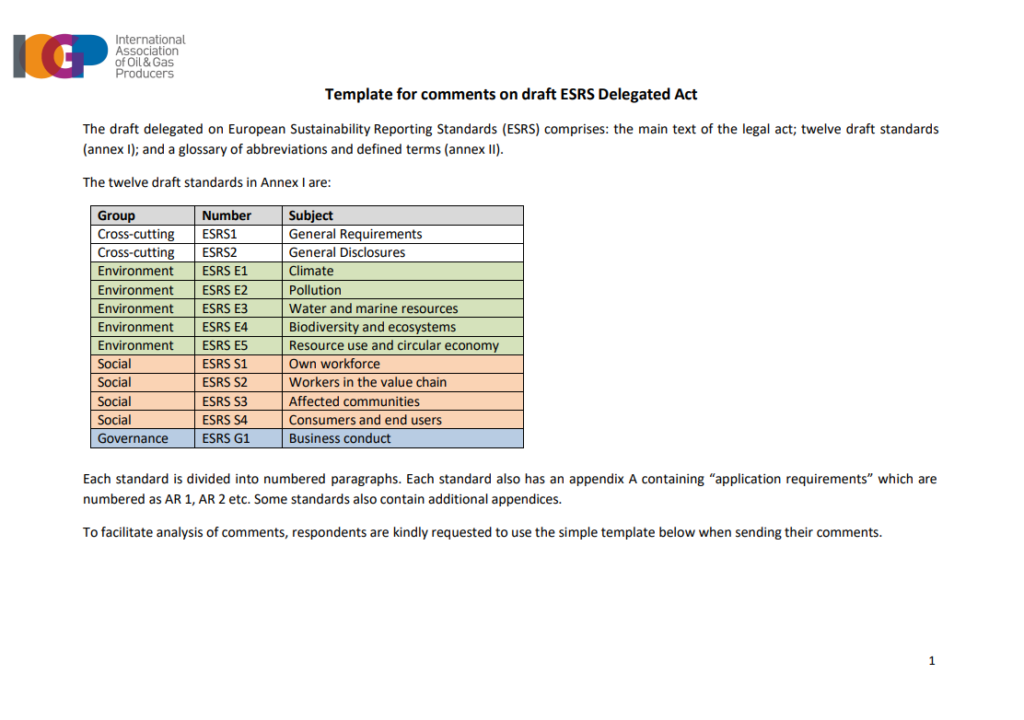

IOGP Europe response to the European Commission’s consultation on the revised Sector Agnostic ESRS

IOGP Europe’s response to the European Chemical Agency’s (ECHA) Socio-Economic Committee (SEAC) draft Opinion of the proposed ‘Universal-PFAS

Socio-Economic Analysis for a Reach Restriction Proposal on PFAS in the Upstream Oil & Gas, Oil Refining and Fuel Distribution Sectors, and in Carbon Capture and Storage

IOGP Europe response to EU Taxonomy Consultation on the Technical Screening Criteria Delegated Act amending the Climate Delegated Act

Delivering on the Omnibus I simplification mandate: IOGP Europe position on the draft Sector-Agnostic European Sustainability Reporting Standards (ESRS)

IOGP Europe response to the EU Taxonomy – review of Climate and Environmental Delegated Acts consultation

Joint industry letter ahead of the plenary vote on the First Omnibus Simplification Package

Amended ESRS Exposure Draft July 2025 Public Consultation Survey

IOGP Europe response to ESMA Consultation on the draft technical standards under the ESG Ratings Regulation

Omnibus Simplification Package: Open Letter with Eurogas and FuelsEurope

Simplification Omnibus Package: towards a proportionate, coherent and efficient sustainability framework for European competitiveness

Joint Position Paper – Extending the ‘Stop-the-Clock’ Initiative to Wave 1 Companies

IOGP Europe Response to the Consultation on the Review of the Taxonomy Climate Delegated Act

IOGP Europe recommendations for the Omnibus proposal

Joint Trade Association Statement: Towards EU due diligence that works for all

EU Taxonomy Stakeholder Request Mechanism

IOGP consultation response to draft EFRAG Value Chain Implementation Guidance (VCIG)

Download

IOGP consultation response: Rationalisation of reporting requirements

Joint industry statement on the EU Taxonomy

IOGP Europe views on the EU corporate sustainability reporting framework

IOGP input on the EU Commission’s public consultation on the EU Taxonomy Delegated Acts

IOGP position on capital requirements

IOGP position on the Corporate Sustainability Due Diligence Directive (CSDDD)

IOGP feedback on the Platform on Sustainable Finance’s draft report on preliminary recommendations for technical screening criteria for the EU taxonomy

IOGP feedback on the Platform on Sustainable Finance’s draft report on social taxonomy

IOGP feedback on the Platform on Sustainable Finance’s draft proposal for an extended taxonomy to support economic transition

IOGP position on the European Commission proposal on the update of the Corporate Sustainability Reporting Directive

FuelsEurope and IOGP position on the Draft Delegated Regulation on taxonomy related disclosures by undertakings reporting non-financial information

IOGP response to the roadmap on the modification of the General Block Exemption Regulation (GBER)

Response to consultation on proposal for an Initiative on Sustainable Corporate Governance

Response form for the Consultation Paper on the Draft advice to European Commission under Article 8 of the Taxonomy Regulation

IOGP input to the Commission’s Delegated Regulation establishing the technical screening criteria for economic activities contributing substantially to climate change mitigation or climate change adaptation

IOGP response to the consultation on ESG disclosures under Regulation (EU) 2019/2088

IOGP response to consultation on the renewed Sustainable Finance strategy

IOGP response to the public consultation on the revision of the NFRD

Sustainability reporting guidance for the oil and gas industry

IOGP Initial Feedback to the Taxonomy: Final report of the Technical Expert Group on Sustainable Finance

Response to the inception impact assessment “Commission Delegated Regulation on a climate change mitigation and adaptation taxonomy”

IOGP input to the Impact Inception Assessment on the Revision of the NFRD

Call for feedback on TEG report on EU Taxonomy

IOGP response to the European Commission’s package on sustainable finance Call for a “Talanoa Platform” to guarantee a smart, inclusive and technology-neutral taxonomy

Press Release: European Parliament backs meaningful simplification of sustainability rules

Letter: The EU’s Corporate Sustainability Due Diligence Directive (CSDDD) – IOGP Europe and FuelsEurope recommendations in view of the trialogue negotiations

Inclusion of gas in the Taxonomy Regulation supports EU ambition to reach climate neutrality by 2050

Sustainable Finance Webinars