FAQ

Isn’t phasing out oil & gas the fastest way to become climate neutral?

It took the world nearly 100 years to transition from wood to coal. A precipitated phase out of oil & gas would disrupt the entire global economy which relies on oil & gas for nearly 60% of its energy needs. Gas drives down emission in power generation wherever it replaces coal. Efficiency gains in car engines reduce transport emissions faster than electric vehicle additions. Pursuing the lowest carbon abatement cost and combining different solutions will remain the most effective way to become climate neutral.

What role could oil & gas possibly have in a climate-neutral EU?

While the role of oil & gas will change in a climate-neutral economy, both will retain a strong share of the energy mix and their value to the energy system will in fact rise. As the share of renewables rises, gas will increasingly serve as a power grid balancing solution, in particular for large seasonal variations. As for oil, while its share in transport is expected to fall, its use as feedstock for high-performance petrochemicals will rise in the coming decades.

What does climate neutrality by 2050 really mean?

Climate neutrality is achieved when GHG emissions are reduced to a minimum and all remaining ones are offset. There are many pathways to reach such an objective, with varying impact on our way of life. By making full use of all existing solutions, assets and skills available across sectors of the economy, including those offered by the oil & gas industry, the transition to climate neutrality can be a success while minimising disruption and costs.

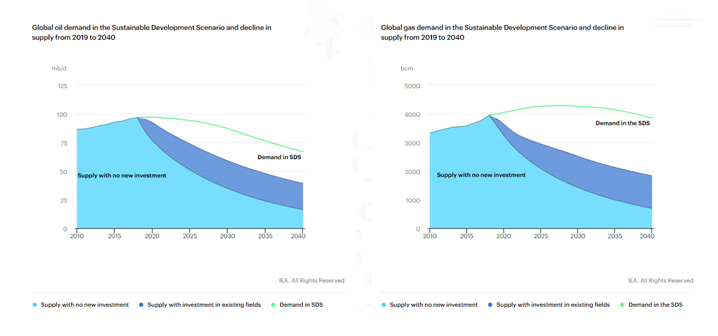

Why don’t we stop investing in oil & gas exploration?

Because even in some of the most ambitious climate scenarios such as the IEA’s Sustainable Development Scenario where oil & gas significantly drops (over 2.5%/year), demand for oil & gas remains strong in absolute terms. If we stop investing in existing and new fields, the natural depletion rate (falling pressure in reservoirs) would lead to a production drop of 8%/year and lead to a shortage on the global market.

Do oil & gas companies invest in non oil and gas activities?

Yes, our member companies supply an increasingly wide range of energy sources and services such as electricity, oil, gas, carbon capture & storage, smart grid management, or carbon offsetting. Some of them operate the largest and most advanced low-carbon energy projects and companies in the world (e.g., Equinor’s doggerbank wind farm; TOTAL’s Sunpower, etc.). The amount of capital investments in low-carbon solutions rises every year, and many companies have rebranded into ‘energy companies’ to reflect this portfolio expansion.

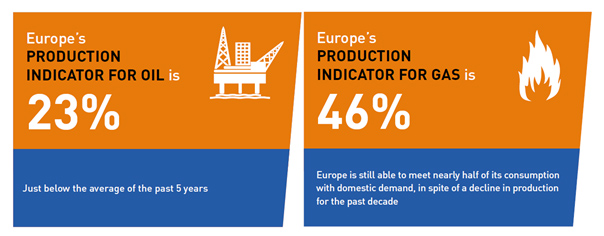

Is there any oil and gas left in Europe?

Yes, Europe still holds vast oil & gas resources. Continued investments in exploration & production in Europe have mitigated the slow decline rate of past years, and allows Europe to produce ½ of the gas and ¼ of the oil the EU needs every year. It is in Europe’s interest to maximise the recovery of these resources to meet its energy needs.